Car Insurance Do I Pay Excess if Not at Fault

Car insurance

Compare car insurance quotes

It's quick and easy to compare car insurance and find cheaper cover – we just need a few details about you and your vehicle.

It only takes a few minutes, and you could save up to £257[1]

-

Tell us a bit about you

Your name, age and where you live, as well as your occupation.

-

Let us know your car details

The make, model and year, as well as any modifications you or previous owners have made.

-

What cover do you need?

How do you use your car? Tell us your annual mileage and choose from fully comp, third-party or third-party fire and theft policies.

Compare car insurance quotes and you could save up to £257 [1]

What type of car insurance do I need?

The best car insurance for you is an affordable policy that covers what you need – don't just pick the cheapest option.

You'll need third party cover as a minimum. It's compulsory, and you can't legally drive without it. But exactly what you're covered for depends on the type of policy you choose.

Comprehensive car insurance

This is the most extensive cover you can get. It covers you for:

- Repair or replacement costs if your car's damaged or written off

- If your car's stolen or catches fire

- Claims made against you for people, passengers and their property.

- It may differ by policy, so check what you're covered for

Find out more about fully comprehensive car insurance

Third party, fire and theft

- This covers you for damage to other people, passengers or their property

- Your car's covered if it gets stolen or damaged by fire too

- If you're responsible for an accident, it won't cover repairs to your vehicle or your own medical costs.

Find out more about third party, fire and theft (TPFT)

Third party only

- This is the most basic level of cover

- It's lowest level of cover you need to legally drive your car in the UK.

- You'll only be covered for damage you cause to other people, passengers, or their property.

- There's no cover for you or your car.

- If your car's stolen, damaged or catches fire you won't be able to claim back the cost.

Find out more about Third party only (TPO)

Join over a million customers with free £250 excess cover^

Claiming on your car insurance is stressful enough, without the added cost of your excess – and we want to help with that.

If you do need to claim, you'll have to pay your excess first, and then we'll refund up to £250 after your claim's settled.

It really is free. We haven't hidden the cost anywhere.

Claim your free £250 excess cover >

^Up to £250 refunded after claim settled. Car insurance purchases only. Excludes breakdown, windscreen and glass repair/replacement. Full T&Cs apply.

Do I need car insurance?

Car insurance is a legal requirement if you're driving in the UK. Find out more about choosing the right cover.

Car insurance for over 50s

Having a wealth of driving experience means car insurance for over 50s is usually cheaper – and there are insurers that offer specialisist insurance too.

More about car insurance for over 50s >

Insurance for new drivers

New and young drivers always pay more. But it doesn't mean you can't get insurance, or you can't get a good deal.

More about new driver insurance >

Learner driver insurance

Learner drivers have a few options for getting covered before taking their test – whether that's in your own car, or someone else's.

More about learner driver insurance >

Join thousands of happy customers who've compared with us[2]

4.8 out of 5

at Trustpilot

Renewal quotes – the easy way to overpay

Don't just settle for the renewal price your insurer sends you. Loyalty doesn't pay – people who stay with their existing insurer almost always pay more than those who switch.[5] A quarter of customers beat their renewal quote by £86.13 with us.[6]Ryan Fulthorpe - GoCompare car insurance expert

[6]25% of customers who provided their car insurance renewal price saved up to £86.13 with Gocompare.com (01 Mar 2021 to 31 May 2021).

How could I get cheaper car insurance?

Car insurance can be expensive, but there are ways you could save money:

-

Pay annually

Paying upfront always works out cheaper than paying monthly, because there's no interest or finance arrangement fee.

-

Tighten up your security

Alarms and immobilisers reduce theft risk. Look for Thatcham-approved devices – some insurers will offer a discount if you have them.

-

Choose a less powerful car

In the market for a new car? Sporty cars with large engines tend to cost more to insure.

-

Drive less miles

The lower your mileage the less you'll pay. But don't underestimate your mileage either – it'll invalidate your insurance.

-

Consider a telematics policy

Telematics insurance policies use a black box or app that tracks your driving to calculate your insurance.

Car insurance that's right for you

If you need anything other than standard car insurance, we've got lots of different policies for you to pick from.

Multi-car insurance

Multi-car insurance can work out easier and cheaper if you've got more than one car to insure.

More about multi-car insurance >

Short-term car insurance

If you only need to drive every now and again or for less than a month, short-term car insurance could work out cheaper.

More about short-term car insurance >

Classic car cover

For additional cover – like spare parts, salvage retention and agreed value – protect your vintage vehicle with classic car insurance.

More about classic car cover >

Business car insurance

If you use your car for work, you'll need the right insurance to be properly covered. There are three different classes of business use you'll need to pick from.

More about business car insurance >

Gap insurance

It's intended to pay the difference between what you paid for your vehicle and what your insurer pays out in the event of a total loss or write off.

More about gap insurance >

Car insurance - Upgrades and additional cover

There are some optional extras you can add to your car insurance. There'll probably be a charge for them, so only add what you actually need.

-

Choose from three levels of cover – roadside assistance, roadside assistance and recovery or roadside, recovery and home start.

It's often cheaper to buy your breakdown cover separately from your car insurance, so make sure you're getting value for money by comparing it on its own.

Find out more about breakdown cover

-

If your car's damaged because of an accident, your insurer can provide a courtesy car while it's being repaired.

You'll have to use one of its approved repairers and check for exclusions.

More about courtesy car cover

-

Legal assistance helps you claim from the person responsible if you're involved in an accident and it's not your fault.

It'll also help to pay to defend a claim brought against you.

More about legal expenses cover

-

If you lose your keys, or they get stolen, lost key cover can help with the cost of replacing them.

Getting high-tech keys replaced can easily run to hundreds of pounds

More about replacement of keys cover

-

Covers the costs of draining and cleaning your tank if you've put in the wrong type of fuel.

It probably won't cover the costs of damage to your engine if you drive away.

More about misfuelling cover

-

For every year you drive claim-free, you'll get a discount on your car insurance.

It's valuable and has such an impact on the price of your insurance that you can protect it. That way, if you need to claim, it won't reduce your no claims history.

More about no claims bonuses and discounts

-

Personal accident cover compensates you for injuries caused by a car accident.

The claim limit varies between insurers, and other drivers and passengers are sometimes covered too.

You'd only claim on personal accident cover if the accident is your fault. That's because if an accident isn't your fault, the at-fault person's insurer will pay out for any personal injury claims.

More about personal injury cover

-

Covers the repair of chips and cracks to your car's windscreen – sometimes it's a free extra.

It can also cover the replacement of your windscreen if it can't be repaired, but you might have to pay an excess.

More about windscreen repair cover

How much does car insurance cost?

Insurers use statistics to work out how likely you are to make a claim on your car insurance – and that's what sets the price.

10% of customers were quoted annual car insurance premiums of £215.50 or less with GoCompare.[3] But we found that our customers pay £468 on average for their car insurance.*

But it varies between cover types. The average price of a comprehensive policy is £458. Third party, fire and theft (TPFT) is considerably more at £628, and third party only (TPO) is more again, at £857.

These are just averages though – your quotes will depend on a lot more than just the cover type you choose. Your age, the car you drive, mileage and driving history all play a part.

If you're a new or younger driver, you'll probably pay more. To insurers, you pose the highest risk, so your premiums will be higher. The average comprehensive price for a 17-year-old is £679.

[3]10% of customers were quoted annual car insurance premiums of £206.50 or less with Gocompare.com (01 Mar 2021 to 31 May 2021).

*The average cost of annual car insurance by policy type purchased in April 2021 through GoCompare. For all types it was £468.59. For comprehensive it was £458.65. For third party fire and theft it was £628.30. For third party only it was £857.19. For all types for 17-year-olds it was £679.14.

Frequently asked questions

-

You don't need to tell your current insurer if the miles you drive have increased or decreased because of coronavirus – for example, because you now drive to work instead of getting public transport, or because you currently work from home.

For new quotes, if how you use your car has changed – and you think it'll stay that way – update your details. A good example is if your mileage will be reduced over the next 12 months. You could get a better price.

Find more information about the effects of coronavirus on your car insurance.

-

You need to be accurate and honest when you declare your annual mileage to get car insurance quotes.

Put in a mileage that's too low and you risk invalidating your cover, which could cause problems if you need to make a claim.

But if you put a higher mileage than you actually drive, you risk paying too much.

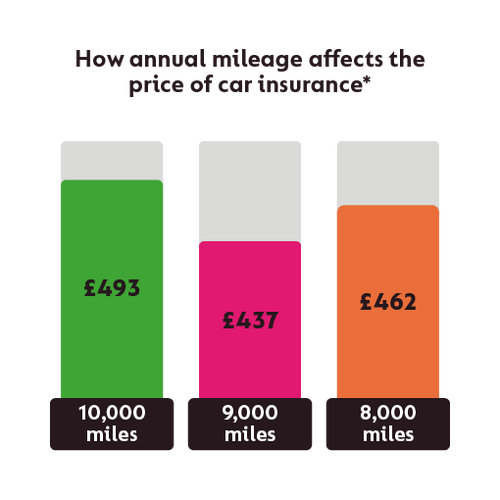

According to our research, car insurance is 13% cheaper if your mileage is 9,000 a year compared to 10,000.

You can check your past MOT certificates to see how many miles you've driven previously. Or try our mileage calculator.

*Average price paid annually for comprehensive car insurance, split by mileage, in April 2021.

-

The impact of your job title on how much your car insurance costs relates to risk factors. So if your job is seen as higher risk by insurers, this is reflected in your premiums. Don't change your job title to try to reduce the price of your quotes, unless the alternative title genuinely describes your job accurately. Always be honest – if you lie you could invalidate your cover.

-

When you get a quote, we'll help you by estimating what your car's worth based on its age and mileage – but you can change it if it doesn't seem right. There are tools online that can help you work out your car's value. Always give an honest valuation. A ballpark estimate's okay because insurer's usually pay out based on average market value.

-

Use our annual mileage calculator to help work out your annual mileage. It'll give you a general idea of your mileage, then you can add a bit more if you need to for irregular journeys and extras, like long driving trips for holidays.

Your annual mileage should be the total mileage for the car, so you need to include miles for all drivers who use it.

You want to get this right – it makes a big difference to the price you'll pay for your insurance. Overestimate your mileage and you'll end up paying too much. Underestimate and you could invalidate your policy.

If you've had your car for over a year and you drive in a regular pattern, you can look at previous MOT certificates or service records to work it out.

-

Some insurers use 'real-time' pricing and others will honour the price they offer for anywhere between 10 and 30 days. When you get quotes with us, we can't guarantee you'll get the same price if you come back later so your quote could go up. Insurers can change their prices at any time.

It usually pays to get quotes a few weeks ahead of your renewal, and lock in a good deal early.

-

Sometimes, but it depends on what cover you've got and how much experience you have driving.

Some insurers offer cover to drive other cars as part of fully comprehensive policies, but it's rarely a feature of third party or third party, fire and theft – and is often written out of policies for young or inexperienced drivers.

Check policy docs to be certain. Often, it's only supposed to be used in emergencies, rather than everyday driving. If you're in any doubt, just call the insurer and ask.

-

This is a bonus (or discount) on your car insurance for every year you've driven and not made a claim.

Find out more about no-claims discounts.

-

An excess is the amount of money you agreed to pay towards a claim when you took out your car insurance.

Generally, an excess is only payable for your damages and when you're at fault. It's usually paid upfront to get the claim process started.

The excess is split into two types; compulsory (set by the insurer) and voluntary (set by you). You don't need to have a voluntary excess, but it might lower the cost of your car insurance if you do.

You'll have to pay both the voluntary and compulsory excess if you make a claim, so make sure the total amount is affordable.

Find out more about car insurance excess

-

As long as you've made a Statutory Off-Road Notification (SORN) for your car, you don't need to have car insurance while it's off the road. But you can still protect your car with laid up insurance, which covers it for fire and theft while your vehicle has a SORN.

-

Insures will run a credit check if you choose to pay monthly for your car insurance, which can leave a mark on your credit score. You're asking for credit, and basically taking a loan, so they do have to run affordability checks. If you pay annually (in one lump sum) a credit check will not be performed when you take out car insurance

-

Unfortunately, if you claim on your insurance, your premiums usually go up the next year.

If you've had, or caused, any accident or damage in the last five years, you need to let insurers know. Even if you didn't make a claim and regardless of blame.

-

If you cancel your policy within the cooling-off period you'll be refunded, less any time you've been covered for already. Some insurers will charge an admin fee for this.

When you're charged for any cover you've already had, it'll be charged pro-rata, so a fair proportion of the entire annual cost of your policy

Cancelling outside of the cooling-off period isn't much different. Some insurers charge a cancellation fee, others don't. Any refund you get will be based on the number of days' cover you've already had.

-

Unless you make changes to your policy, cancel it or need replacement documents, you shouldn't have to pay any admin fees.

If you do need to change something, like your address, car, registration, or adding a driver, most insurers will charge you an adjustment fee. Some might let you make basic changes online without charging you, while others won't. There's no standard flat fee, insurers can charge whatever they like.

When you're comparing policies, look out for admin fees. They add up, so it's worth factoring them in.

-

- If another driver or person is involved, exchange details

- Make notes about what happened and take pictures as evidence

- Let your insurer know within 24 hours

- You'll need to fill in a claims form and possibly have your car assessed for damage

- Pay your excess – your claim won't be processed until you do

Your insurer will settle the claim if it's clearly your fault. If the other driver's at fault or it's not obvious who's to blame your insurer and the insurers of other driver involved will look at the evidence, decide who's at fault and settle the claim.

When both parties are to blame, or if a decision can't be agreed, your insurers will split the claim between them.

If you weren't at fault and the other driver's insurer settles the claim costs your insurer will give you your excess back.

Beware, your claim might be refused if:

- You provide incorrect or misleading information

- The main driver isn't who you said it'd be when you took out the policy (this is called fronting, it's illegal)

- The accident was caused by your negligence or by your car being unroadworthy

- You don't have any proof

- You file your claim too late

Find out more about making a claim on your car insurance and typical reasons claims get rejected, and how to avoid it happening.

-

Yes - you don't have to claim on your insurance if you don't want to but you still need to tell your insurer about the accident.

You can make it clear that it is for information purposes only, and that you're not looking to make a claim.

Make sure you notify your insurer about the incident within a reasonable timeframe (this might be specified in your policy so check the wording). If a timeframe is not stated, get in touch with your insurer as soon as possible.

Load more

Customer reviews

Whenever I need to find valuable car insurance, GoCompare makes life easier for me therefore I am a loyal customer for some years now! Thanks GoCompare!

Offered me a better date than other comparison sites and don't hassle you by phoning up

So easy to compare & then purchase car insurance …. Should have done it years ago!

Got a cheaper quote and saved money for my car insurance

GoCompare uses cookies. By using the website you agree with our use of cookies.

Continue

Car Insurance Do I Pay Excess if Not at Fault

Source: https://www.gocompare.com/car-insurance/